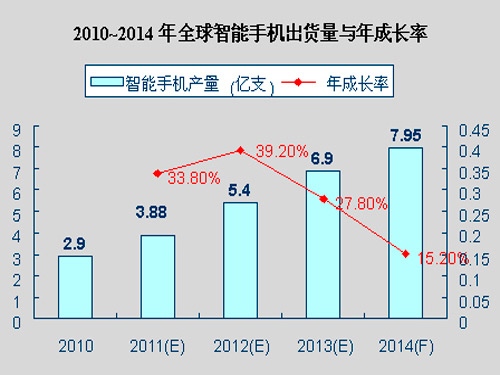

Global smartphone shipment growth will reach 33.8% in 2011, of which the Asian region will account for 27.8% of global mobile phone shipments, which will replace 27% of North America and become the largest region for global smartphone shipments, while China In 2011, it is expected to sell more than 100 million smartphones. With the rising income of the Chinese and Indian people, and the gradual popularity of local 3G network construction, it will give rise to consumers’ further functional demand for mobile phones. Tuo estimates that emerging markets such as China and India will be the next one. The important battlefield of the mobile phone industry.

Global smartphone shipment growth will reach 33.8% in 2011, of which the Asian region will account for 27.8% of global mobile phone shipments, which will replace 27% of North America and become the largest region for global smartphone shipments, while China In 2011, it is expected to sell more than 100 million smartphones. With the rising income of the Chinese and Indian people, and the gradual popularity of local 3G network construction, it will give rise to consumers’ further functional demand for mobile phones. Tuo estimates that emerging markets such as China and India will be the next one. The important battlefield of the mobile phone industry. According to Xie Yushan, assistant director of the Communication Research Center of TPI, the brand manufacturers are eager to develop mid-to-low-end smartphone products in addition to continuing to create high-end smartphone peaks in mature markets and collaborating with chip makers. Attacking potential consumers who are still using feature phones will fully pull the mobile front into the smart battlefield. Topo predicts that under the fast background of low-end and mid-tier smartphones and the rapid deployment of 4G infrastructure in Asia, the brand makers will not only push up the demand for mobile intelligent terminal products in emerging markets, but also become global intelligence. The door of the mobile phone market is open, and software revenue will generate considerable long-term benefits for business operations.

The market price of smartphones is a key factor for civilians. As the growth rate of high-end smartphones in the mature market gradually slows down, from the second half of 2011, the growth center of smart phone market will shift from developed countries to emerging markets and move from high-end smartphones. To low-end smart phones. Since the global smartphone penetration rate was 26% in 2011, the penetration rates of smart phones in the United States and Europe were 51% and 34%, respectively, and that in Mainland China was 30.64%. Topo said that price will be a key factor in expanding more demand for smart phones, and low prices will drive the current surviving of more than 60% of the world's functional mobile phone users into smart phones. Therefore, the low-end mobile phone or operator's promotion strategy , will be able to effectively drive from the function to intelligent mobile phone replacement surge.

Taking the Chinese mainland market as an example, the three major operators from China Mobile, China Unicom, and China Telecom have strengthened their terminal subsidy and have directly boosted sales of smart phones in mainland China. Tuo pointed out that in 2010, the sales volume of smartphones in mainland China reached 80 million, including about 10 million smartphones. It is estimated that the sales of smartphones in 2011 will reach 110 million, and the annual growth rate will be 37.5. %. With the boom of GPhone, OPhone, entry, and cottage smartphones, and the shift in the consumer market structure in mainland China, the strategy of popularizing smart phones will be an important stepping stone for local consumers to switch to smart phones. In order to open up the doors of emerging markets such as China, the deployment of mobile broadband networks will be more effective.

Takuma estimates that the number of mobile subscribers covered by the global mobile broadband market in 2011 will have doubled compared to 2009, reaching 1 billion subscribers. The dramatic jump in mobile network users will directly drive the plans for telecom operators to upgrade their existing networks to 4G LTE. Demand for explosive growth, which is the strongest construction of the Asian market. Takuya predicts that the Asian region will set off a new wave of smart phone wars, and Nokia, which has taken a firm foot position in the feature phone market, will have a chance to make a comeback as long as the existing functional mobile phone loyal users shift to use low-end and mid-range smart phones. In addition, through the cooperation with Microsoft, there is also an opportunity for Nokia to open another window in the commercial market.

The chip factory is investing in low-end smartphones born of low-end smart phones. With plans from various international brand manufacturers such as HTC, Samsung, Motorola, etc., as well as Android open platform resources, heavyweight chip makers such as MediaTek will also be in 2011. The introduction of mid-to-low-end smart phone chip solutions not only gradually overlaps with Qualcomm's product line, but also actively acquires wireless communication chip factories and touch IC factories. The attitude of low-end and middle-end smart phones is obvious; the international giant ST-Ericsson also In April 2010, it demonstrated that its product layout is different from previous attempts. From high-end dual-core smartphone chip platforms to low-end smart chips, the product layout can be seen. Takuma estimates that, with the support of brand manufacturers and chip makers, global low-end smart phone shipments will rapidly rise to 40 million in 2011, and it is expected to grow to 150 million in 2012, accounting for a significant increase. The overall proportion of smart phones reaches 30%.

Takuya said that once the price of smart phones falls below 200 US dollars, it can be expected to follow the footsteps of mobile phone development in the 1990s and be popularized. If the price is close to 100 US dollars, it is the key to fully start the emerging market. As the development of smart phones will inevitably squeeze the existing human resources of the mobile phone brand factory, mobile phone brand factories will rely more on mobile phone ODM plant research and development support than in the past, and low-end smart phones will compress the existing high-end products. The profitable space will be highlighted by the cost control advantages of Taiwan's mobile handset foundries. Takuya predicts that in addition to the possible opening of the middle and low-end smartphone market portals, in addition to the possible impact on the layout of brand manufacturers, Taiwan's mobile phone OEMs must also adjust the OEM strategy and strengthen the technical level to respond to smart phone battles. A cup of soup.

Global Smartphone Shipment and Annual Growth Rate from 2010 to 2014

ZHW Technology Co., Ltd. , http://www.gdfiberadapter.com